LIFO is only allowed in the USA, whereas, in the world, companies use FIFO. In the USA, companies prefer to use LIFO because it can help them reduce their taxable income. Furthermore, when USA companies have operations outside their country of origin, they present a section where the overseas inventory registered by FIFO is modified to LIFO. You can also check FIFO and LIFO calculators at the Omni Calculator website to learn what happens in inflationary/deflationary environments. Considering these pros and cons will help you determine whether implementing a perpetual inventory system is right for your business operations. A perpetual inventory system offers several advantages for businesses, but it also comes with some drawbacks.

How Is Inventory Tracked Under a Perpetual Inventory System?

Under a periodic LIFO system, however, layers are only stripped away at the end of the period, so that only the very last layers are depleted. The periodic system is a quicker alternative to finding the LIFO value of ending inventory. The reason for organizing the inventory balance is to make it easier to locate which inventory was acquired most recently. know the facts about the fair tax Lastly, we need to record the closing balance of inventory in the last column of the inventory schedule. Based on the calculation above, Lynda’s ending inventory works out to be $2,300 at the end of the six days. Last In First Out (LIFO) is the assumption that the most recent inventory received by a business is issued first to its customers.

LIFO, Inflation, and Net Income

First, the software credits the sales account and debits the accounts receivable or cash. Second, the software debits the COGS for the merchandise and credits the inventory account. In this section, we will discuss some of the key formulas used in perpetual inventory systems to help businesses effectively manage their stock levels and make informed decisions. These formulas include COGS, economic order quantity (EOQ), weighted average cost, and gross profit.

How To Calculate FIFO

The two systems also differ in how they calculate Cost of Goods Sold (COGS). In a perpetual inventory system, COGS is calculated automatically after each sale by multiplying the number of units sold by their respective costs per unit (source). Conversely, in a periodic inventory system, COGS is determined manually at specific intervals using beginning and ending inventories along with purchases made during that period. The cost of goods sold, inventory, and gross margin shown in Figure 10.19 were determined from the previously-stated data, particular to perpetual, AVG costing. Regardless of which cost assumption is chosen, recording inventory sales using the perpetual method involves recording both the revenue and the cost from the transaction for each individual sale.

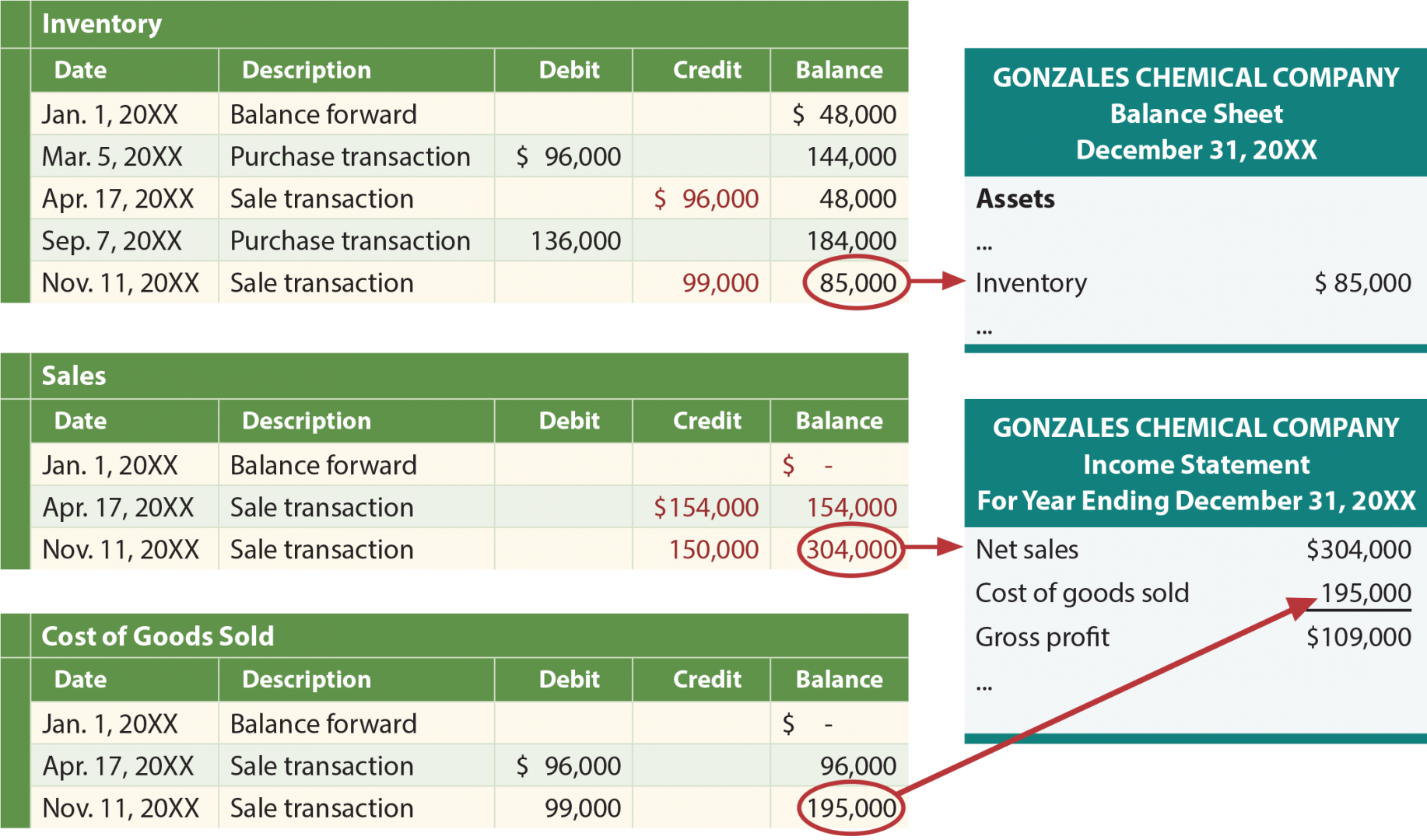

Calculations of Costs of Goods Sold, Ending Inventory, and Gross Margin, Specific Identification

- Physical flow is which you know if we’re selling cans of soda, which can can of soda we are actually selling?

- The 220 lamps Lee has not yet sold would still be considered inventory, and their value would be based on the prices not yet used in the calculation.

- For example, on the first day, 10 units of inventory were added at the cost of $500 each, which we will record as follows.

- Also, all the current asset-related ratios will be affected because of the change in inventory value.

- To facilitate this process, many organizations rely on specialized inventory management software.

Products are barcoded, and point-of-sale (POS) technology tracks these products from shelf to sale. These barcodes give companies all the information they need about specific products, including how long they sat on shelves before they were purchased. Perpetual systems also keep accurate records about the cost of goods sold (COGS) and purchases. This card shows the starting inventory, sales, purchases, prices and balances. Under a perpetual system, inventory records for this product are continually changing. When the company sells merchandise, the perpetual software records two transactions.

The first-in, first-out method (FIFO) of cost allocation assumes that the earliest units purchased are also the first units sold. Once those units were sold, there remained 30 more units of beginning inventory. At the time of the second sale of 180 units, the FIFO assumption directs the company to cost out the last 30 units of the beginning inventory, plus 150 of the units that had been purchased for $27. Thus, after two sales, there remained 75 units of inventory that had cost the company $27 each.

Even if you’re using a spreadsheet, adding new layers and modifying existing layers takes a lot of data entry and cleaning up. This is the reason why some prefer the periodic inventory system because of its simplicity. In our last transaction above, we withdraw inventory costs from three different layers.

As indicated by the name itself, the LIFO method bases the COGS on the cost of the most recent purchases (last in). It means that recently purchased goods are expected to be expensed first or transferred to the COGS. LIFO reserve refers to the amount by which your business’s taxable income has been reduced as compared to the FIFO method. If Kelly’s Flower Shop uses LIFO, it will calculate COGS based on the price of the items it purchased in March.